Open Banking

How Nectar is joining the latest financial innovation

Open Banking

How Nectar is joining the latest financial innovation

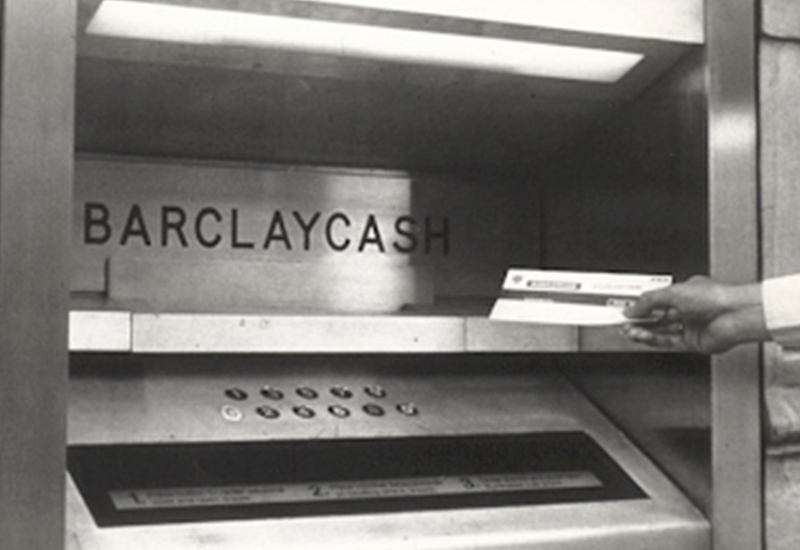

On 27 June 1967, the world’s first automated teller machine (ATM for short, but more commonly known in the UK as a cashpoint) was unveiled at a branch of Barclays Bank in Enfield, north London. Barclays’ then deputy chairman was given the honour of drawing back a velvet curtain, while comedy actor Reg Varney, best known for the sitcom On the Buses, made the first withdrawal of £10 – the maximum permitted for a single transaction.

Up until this point, you could only get cash out of your bank account during bank branch opening hours, typically weekdays 9.30am to 3.30pm.

Fast-forward half a century and there are now around 70,000 ATMs in the UK, with each machine dispensing, on average, £2.5m of cash every year. 23 December 2016 holds the record for the most cash withdrawn in a single day at a massive £730m. Must’ve been all that last-minute Christmas shopping!

Learning to trust the machines

What has been largely forgotten in the years since is that, when ATMs were first introduced, the public didn’t really trust them.

The trust that customers had in allowing a bank teller to withdraw funds from their account was so ingrained that the thought of a machine offering the same service seemed unacceptable. Surely these machines would make a mistake and customers would be out of pocket.

But all innovation, particularly in financial services, comes with a period of adoption and initial hesitation often focussed on trust and security. ATMs are now an icon of convenience and an intrinsic part of the fabric of our everyday lives – so it’s safe to say those initial trust issues have long since subsided.

What is Open Banking?

Open Banking regulations were introduced in the UK in 2018 on the back of the EU-initiated Payments Services Directive 2 (known as PSD2). It was an attempt to bring more competition and innovation to financial services, as well as giving customers more rights over their transaction data, and it was championed by the Competition & Markets Authority. To date, around 2.5 million UK customers have signed up to an Open Banking-enabled service, so it’s an innovation that’s still waiting for a catalyst to really scale it up in this country. Other countries are following the UK’s lead, with momentum building in Australia, Japan and the USA.

What does Open Banking bring to the table?

In customer terms, this deregulatory move in the banking sector now allows an individual to grant a trusted third-party (TTP) organisation permission to view their payment transactions by linking their payment account(s) to that organisation. This opens up pipes into the relevant Bank or Card Issuer, allowing transaction data to be passed via API to the TTP. This data can then be processed, analysed and used in multiple ways. The most common examples of Open Banking-enabled customer propositions around today include:

Aggregation

Allows you to aggregate credit and debit card account information from multiple providers to display it all in one place, which, in turn, enables spending analysis and support in setting savings goals.

Affordability

Gives banks and credit providers access to banking transaction data to help them make more informed lending decisions based on affordability and credit risk, opening up the opportunity to pre-approve customers for a line of credit if and when they need it.

Advice

Allows you to provide an immediate and accurate view of your debt picture to an advice platform, helping you get the best support if you find yourself in a debt management situation.

Application

Speeds up the mortgage application process by removing the need for you to send physical bank statements.

Action

Understand how your spending choices (where you spend and how much you spend) can impact your personal carbon footprint.

Auto-switching

Allows third-party switching services to view your direct debits for insurance, utilities and other household services to assess whether better deals are available, and switches to them for you.

Auto-saving

Offers a ‘round-up’ proposition where the ‘change’ from a debit card transaction (the difference between the transaction amount and the next whole pound value) is calculated and transferred into your savings or investment account, or donated to charity.

Meet Nectar Connect

Nectar’s new Open Banking-powered Nectar Connect proposition

Nectar’s new Open Banking-powered Nectar Connect proposition adds another example to this list – one that we hope will act as the catalyst to wider acceptance and adoption. Nectar Connect rewards customers according to where they choose to make their day-to-day spend.

The ability to view a customer’s payment transaction data to see allows us to reward them based on our detailed understanding of where they spend, helping them get more for their money. Crucially, no Nectar card swipe is needed to track the transaction and identify the customer, so no merchant POS integration is required.

Unlocking a breadth of new places to earn points, plus the value of the points on offer and the ease with which those points can be collected, empowers Nectar members who sign up to Nectar Connect to substantially boost their points balance, and accelerates them to their next rewarding redemption experience.

We believe that Open Banking will follow a similar trajectory to the ATM. At first, there might be some hesitation and caution among customers, but the benefits will quickly be revealed, and it’ll become a normal part of our lives.

The ATM succeeded because it offered real utility to customers by making their life easier. Open Banking will succeed if it can offer utility, or, like Nectar Connect, deliver real financial value back to customers. And success will mean that in another 50 years’ time, we will look back and find it impossible to imagine life without it.